In India, saving is a common habit among most people. They keep their money into Saving A/c, Fixed Deposits (FD), Recurring Deposits (RD), Post Office, Chit Funds, Life Insurance and Annuity Plans. It hardly gives 3-5.5% return on above investments. In addition, people don’t know or ignore inflation rate which is 4-5%. Eventually, what they are getting is 0-1% returns. Although they don’t want to participate in stock market due to volatility, previous events & scams. So, what are other investment options for people with minimum risk and better returns? Only solution for this is Mutual Funds. It don’t need active participation from investors like stocks. Many investors have created wealth through mutual funds over a period of years.

Generally, many people are confused about SIP and Mutual Funds. Both terms are related to each other. SIP is Systematic Investment Plan in which fixed amount is invested in mutual fund at regular intervals. Currently there are 4.91 crore SIP accounts are active. Monthly SIP collection has touched Rs.11,005 crore in December 2021 (source: Economic Times).

Securities Exchange Board of India (SEBI) is watchdog for mutual fund industry in India. It functions like Reserve Bank of India (RBI) regulating banks in India. SEBI regulates the market & protect the interest of investors. So, investors need not to worry about their invested money or any fraud.

Definition

Mutual Fund is a form of investment vehicle in which investors’ money are collected and Professional Investment Advisor/Fund Manager is hired to manage it. He/she invest that money into different type of securities like Stocks (Equity), Debt (Fixed Income) or Both (Hybrid).

Net Asset Value (NAV)

NAV is a price of units in mutual fund scheme. When AMC (Asset Management Company) brings NFO (New Fund Offer), it offers units at Rs.10/unit. NFO in mutual fund is like IPO in stock market. Its unit value changes on the performance of shares in scheme, expense ratio, dividend reinvestment. It’s value changes at the end of the day. NAV can be calculated by dividing the total net assets by total no. of units issued. So, mathematics formula is: – NAV = (Assets – Liabilities) / Total No. of Outstanding Units

How SIP Works?

Through SIP, unit-holders can invest regularly on monthly/quarterly/half-yearly as per their convenience. Investors only need to exercise auto-debit form once with set amount. From next month, SIP amount gets automatically deducted on given date from bank a/c and invested in market. It is like Recurring Deposit (RD) in bank.

Example: In stock market, there are many stocks which are expensive like MRF (Rs.70,000), Infosys (Rs.1740), Bajaj Finance (Rs.7150), HDFC Bank (Rs.1525), D-Mart (Rs.4100) & so on. Suppose an investor named Ganesh want to invest in stock market but not able to buy such blue-chip company stocks because of limited funds.

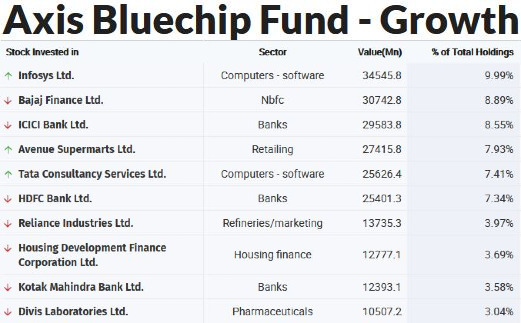

Mutual fund solves this problem. It collects funds from many retail & HNI investors and collectively invest that money into mutual fund schemes with percentage allotted to stocks. Following is the image from Moneycontrol.com of Axis Bluechip Fund scheme:

In above image, if mutual fund company has collected Rs.1,000 each from 100 investors, it has gathered Rs.1,00,000. Then fund manager will allocate this Rs.1,00,000 into companies as per % of holding in the scheme. So, in above scheme, Rs.9,999 (9.99%) will be invested in Infosys, Rs.8,890 (8.89%) in Bajaj Finance, Rs.8,550 (8.55%) in ICICI Bank, Rs.7,930 (7.93%) in D-Mart & so on will be invested. Due to this structure, investors get the benefit of investing in expensive stocks and diversification with minimum amount. Investors can invest with starting of Rs.100 in mutual fund.

Advantages & Disadvantages

| Advantages | Disadvantages |

| Professional Management | High Expense Ratio |

| Diversification | Transaction Costs |

| Low Minimum Investment | Lock-in period for Tax Efficient funds |

| Dividend Reinvestment | Exit Load (if redeemed before certain period) |

| Tax Efficient | Herd Effect |

Returns from Mutual Fund

The overall mutual fund industry average return is considered between 10-12%. However, it totally depends upon scheme performance, period of investment, type of scheme and Total Expense Ratio. For e.g., Historically, small cap funds have delivered 20-25% returns if invested for more than 5 years. Following are the calculation examples: –

1] With only SIP of Rs.2000 invested for 15 years @12%, the amount will grow to Rs.10,09,152.

2] By increasing SIP amount to Rs.3000 @15% for 20 years, the amount will grow to Rs.45,47,865.

3] If same amount invested in Recurring Deposit @6% for 20 years, it would grow to Rs.13,93,053.

You can see the difference of returns between RD & SIP. Also, with only 1-2% increase in return, it results into significant returns over a period of years. It is called Power of Compounding. You can also calculate Mutual Fund returns through following link:- https://groww.in/calculators/sip-calculator

Direct Plan VS Regular Plan

Every mutual fund scheme has 2 plans while investing – Direct & Regular. Following is the difference:

| Direct Plan | Regular Plan |

| Brought from AMC & no Intermediary is involved | Brought through Mutual Fund Distributor |

| We can invest Online on AMC Website & Apps | Mutual Fund Distributor invest our Money |

| No distribution expenses | Distributors receives Commission from AMC |

| Better returns from Regular Plan | Lower returns from Direct Plan |

| Low Total Expense Ratio (TER) | High Total Expense Ratio (TER) |

| Net Asset Value (NAV) is Higher | Net Asset Value (NAV) is Lower |

So, in this post we have seen NAV, basics of mutual fund, how it works with example, its calculation and 2 options while investing in it. In next article, we will see types of mutual fund, its objectives, sub-categories, investing behavior & options to invest.

Useful and amazing information

Thank You Dnyaneshwar Chaugule

Excellent

Thank You Ganesh Pandey

Useful post…very nice

Thank You Nilima

This site is mostly a stroll-by for the entire info you needed about this and didn抰 know who to ask. Glimpse right here, and you抣l undoubtedly discover it.

Wonderful work! This is the type of info that should be shared around the web. Shame on Google for not positioning this post higher! Come on over and visit my web site . Thanks =)

Usefull and informative

Thank you, Swapnil